How Whole Life Insurance Functions as a Hidden Savings Account

Whole life insurance is often misunderstood merely as a safety net for dependents, but it actually serves a dual purpose, functioning as a hidden savings account. Unlike term life insurance, which offers no cash value upon expiration, whole life policies accumulate a cash value over time. This cash value grows at a guaranteed rate, allowing policyholders to build savings while simultaneously providing lifelong coverage. As premiums are paid, a portion goes towards the cash value, which can be accessed in the form of loans or withdrawals, giving policyholders the flexibility to use these funds for emergencies, investment opportunities, or other financial needs.

Moreover, the hidden savings account feature of whole life insurance offers a level of financial security that is often overlooked. The cash value grows on a tax-deferred basis, meaning that you won’t pay taxes on the growth until you withdraw it, which is beneficial for long-term savings strategies. Some policyholders choose to *borrow against* their cash value to finance major expenses like home renovations or educational costs, while still keeping their death benefit intact. This feature makes whole life insurance not just a protection plan, but also a strategic financial tool that can contribute to overall wealth building.

The Financial Benefits of Whole Life Insurance: More than Just Death Benefit

Whole life insurance offers financial benefits that extend well beyond its primary role as a death benefit. One of the most significant advantages is the cash value component that accumulates over time. As policyholders make premium payments, a portion of these funds is allocated to a cash value account, which grows at a guaranteed rate. Unlike term insurance, which provides no cash value, whole life insurance enables individuals to build a cash reserve they can borrow against or withdraw during their lifetime. This can be advantageous for those looking to finance important milestones such as education expenses or purchasing a home.

Additionally, whole life insurance policies provide a level of stability and predictability in an individual’s financial planning. The death benefit is guaranteed and remains fixed as long as premiums are paid, which can serve as a source of financial security for loved ones. Moreover, the cash value grows tax-deferred, allowing policyholders to sidestep immediate tax liabilities on earnings. This tax advantage, coupled with the policy's capacity to provide liquidity and flexibility through loans or partial withdrawals, positions whole life insurance as a valuable tool in comprehensive financial strategizing.

Is Whole Life Insurance a Smart Investment Strategy for Your Future?

When considering your financial future, the question of whether whole life insurance is a smart investment strategy often arises. This type of policy not only provides a death benefit to your beneficiaries but also accumulates cash value over time. Unlike term insurance, which merely offers coverage for a specific period, whole life policies are designed to last a lifetime, offering both protection and a potential source of savings. The cash value component grows at a guaranteed rate, allowing policyholders to borrow against it, which can be a strategic way to fund major expenses such as education or retirement.

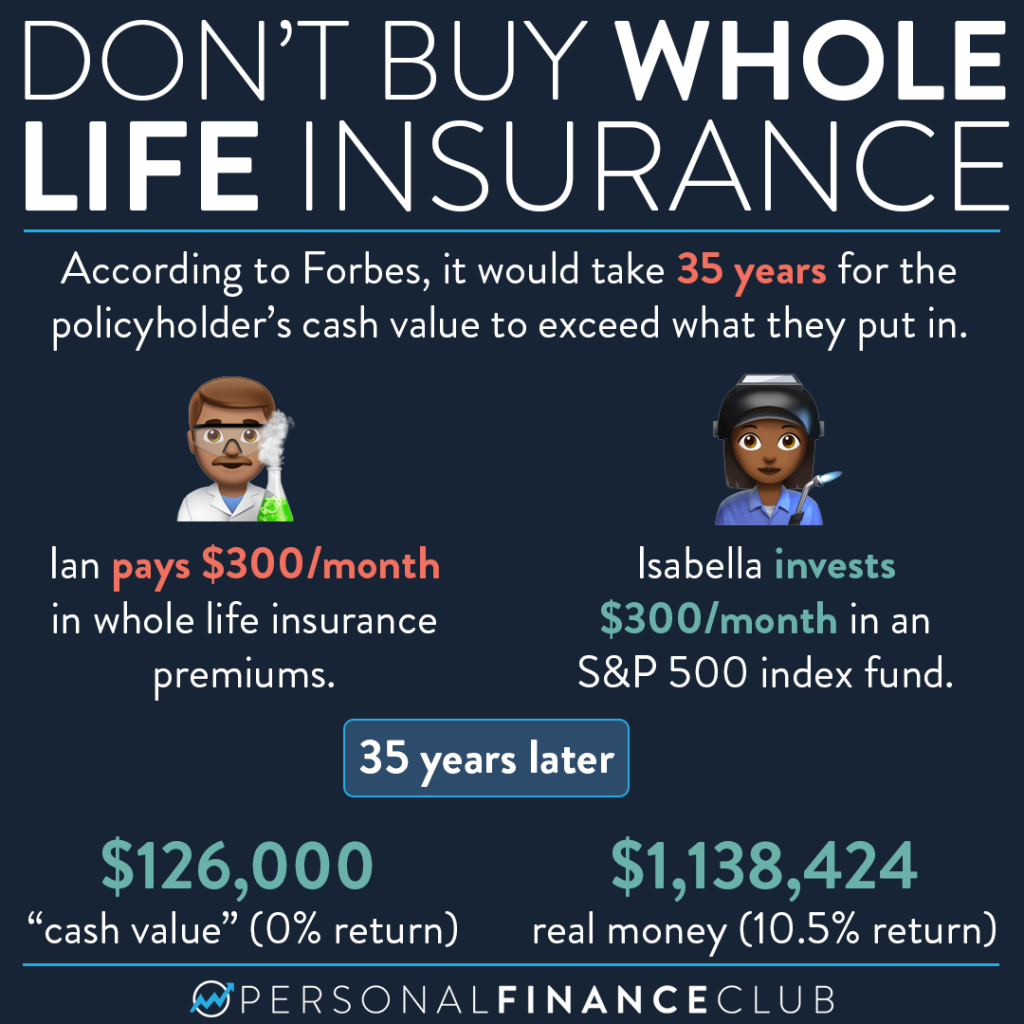

However, it's essential to weigh the benefits against the costs. Whole life insurance premiums tend to be higher than those of term policies, which can make it less suitable for everyone, especially those on a tight budget. Some financial experts argue that investing in traditional savings or investment vehicles might yield a higher return than the cash value accumulation offered by whole life policies. Therefore, it's crucial to examine your financial goals and consult with a financial advisor to determine if whole life insurance aligns with your overall investment strategy and future financial needs.