Understanding the Basics: What is Term Life Insurance?

Term life insurance is a type of life insurance policy that provides coverage for a specified period, typically ranging from 10 to 30 years. It is designed to pay a death benefit to the policyholder's beneficiaries if the insured person passes away during the term of the policy. One of the significant advantages of term life insurance is that it is generally more affordable than permanent life insurance, making it an attractive option for individuals looking to secure financial protection for their loved ones without breaking the bank. Additionally, policyholders can choose the coverage amount that best suits their needs and budget, offering flexibility in their financial planning.

Understanding how term life insurance works is crucial for making an informed decision. When purchasing a term life insurance policy, you typically pay a monthly or annual premium, which remains constant for the duration of the policy. If the insured individual does not pass away within the term, the policy expires, and no benefit is paid out. However, many insurers offer conversion options, allowing policyholders to switch to a permanent policy before the term ends. This feature can provide peace of mind, knowing that you have an option for continued coverage as your circumstances change over time.

Is Term Life Insurance Right for You? Key Considerations to Keep in Mind

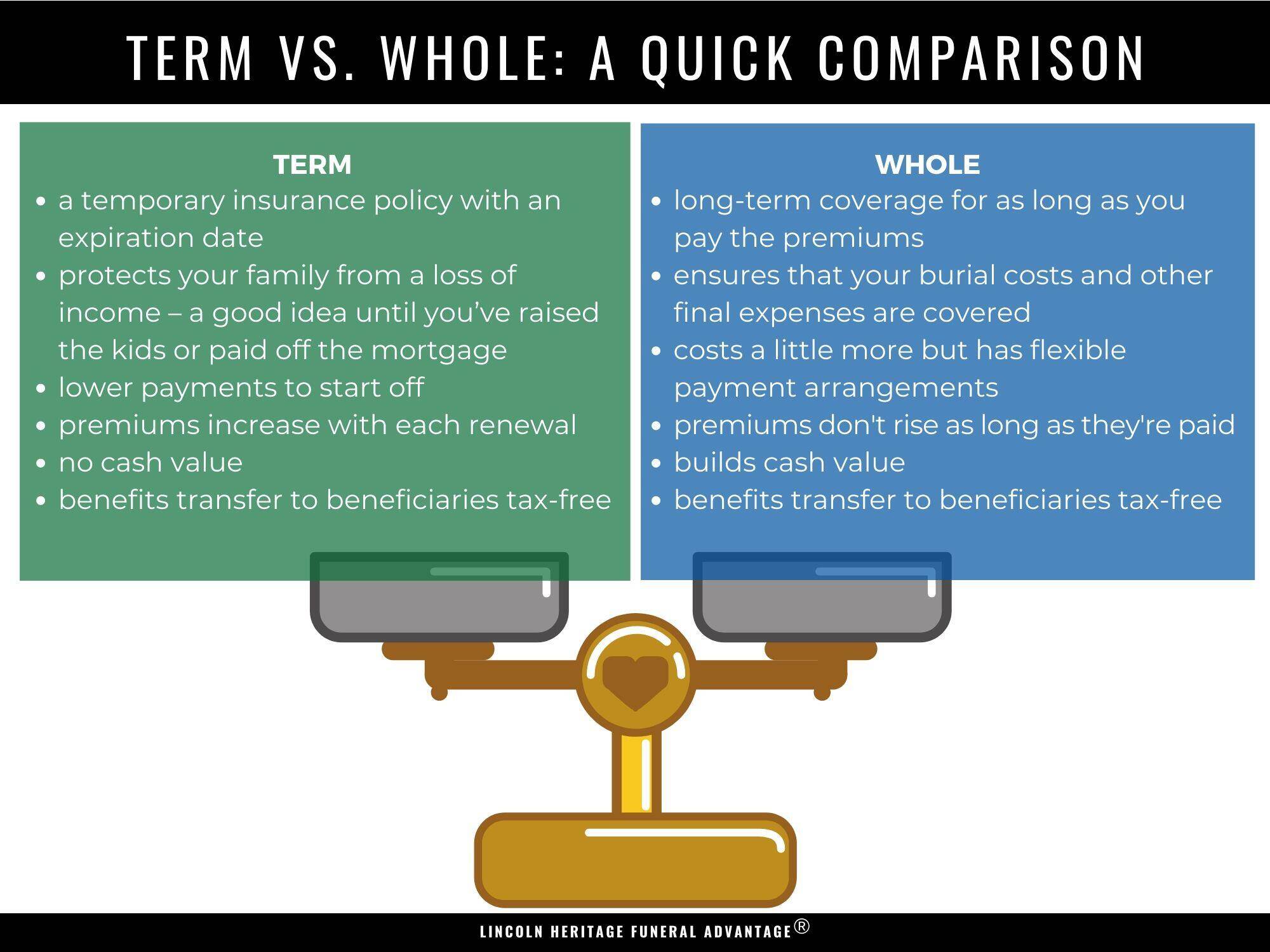

Deciding whether term life insurance is right for you involves assessing your financial needs and future goals. Unlike whole life policies, which provide coverage for your entire life and can accumulate cash value, term life insurance offers protection for a specified period—typically ranging from 10 to 30 years. This can be particularly advantageous if you are looking to cover specific financial responsibilities during your working years, such as paying off a mortgage or funding your children's education. Evaluate your current financial obligations and consider how long you need coverage to determine if a term policy aligns with your needs.

Another important aspect to consider is your budget. Term life insurance tends to have lower premiums compared to other types of life insurance, making it a more affordable option for many individuals and families. However, it is essential to balance the cost with the coverage amount you require. Here are a few key points to consider:

- Assess your current and future financial responsibilities.

- Determine how many years of coverage you will need.

- Compare quotes from multiple insurers to find the best rate.

How Term Life Insurance Works: A Step-by-Step Guide

Term life insurance is a type of life insurance policy that provides coverage for a specified period, usually ranging from 10 to 30 years. The process begins with the policyholder choosing a coverage amount and term length based on their financial needs and the needs of their beneficiaries. Once the application is submitted, the insurer conducts a thorough underwriting process which may include a medical exam to assess the applicant's health risk. Upon approval, the policyholder pays regular premiums, and in return, the insurer agrees to pay a death benefit to the designated beneficiaries if the policyholder passes away within the term of coverage.

As the term nears its end, policyholders have options to consider. They can renew the policy for another term, convert it to a permanent life insurance policy, or simply let it expire. It is important to note that premiums may increase upon renewal, especially as the insured ages or if their health status changes. Understanding these options is crucial for making informed decisions about financial planning and ensuring that loved ones remain protected even in the face of unexpected events.