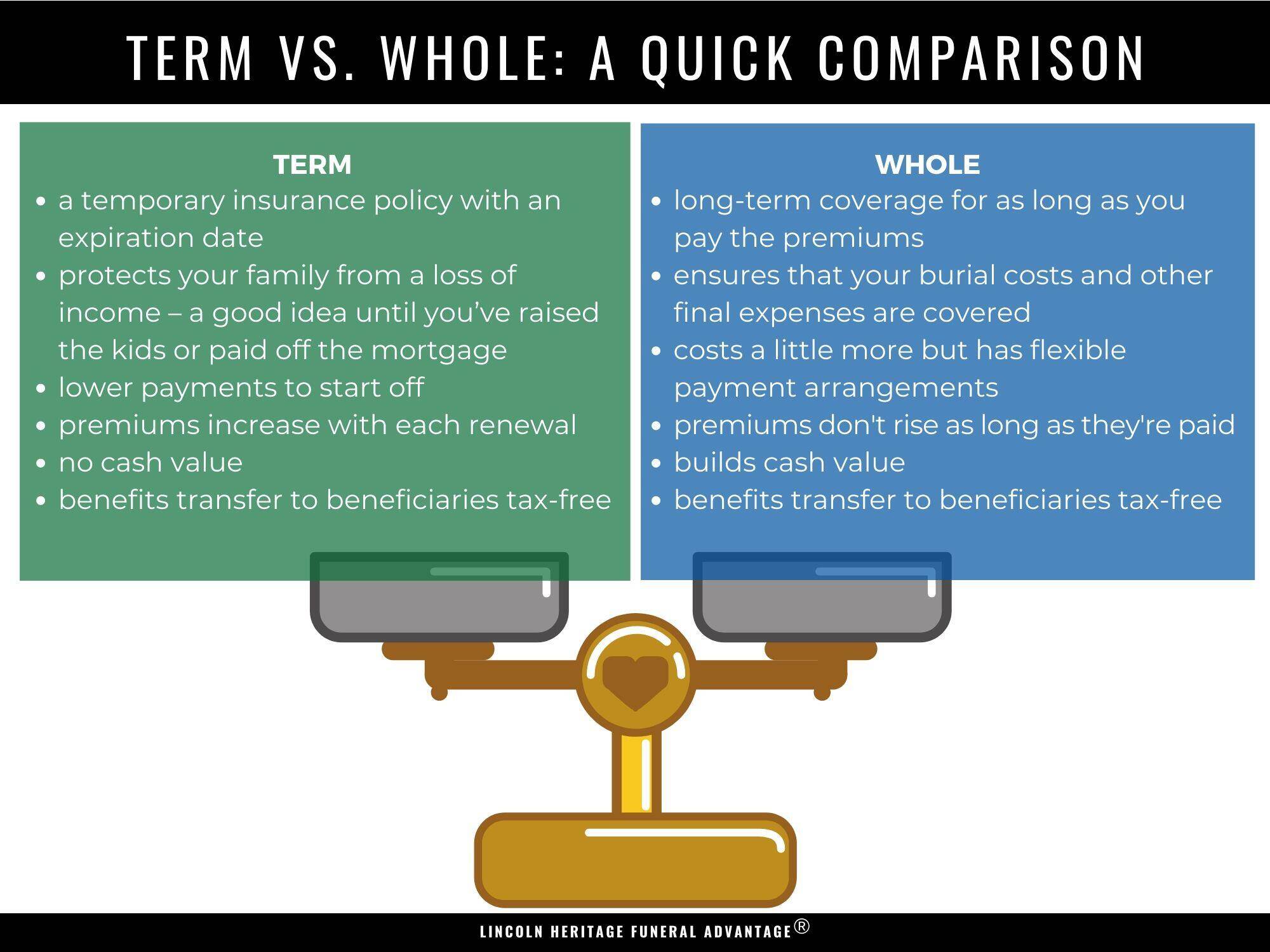

5 Common Whole Life Insurance Myths That Could Drain Your Finances

Whole life insurance is often surrounded by myths that can mislead consumers and impact their financial decisions. One common myth is that whole life insurance is a poor investment compared to other financial products. While it's true that whole life policies are typically more expensive than term life insurance, they provide guaranteed cash value accumulation and lifelong coverage. This aspect makes them a stable part of a diversified financial strategy, rather than just an expensive burden.

Another prevalent misconception is that whole life insurance is only for the wealthy. In reality, individuals from various financial backgrounds can benefit from whole life insurance, thanks to customizable premium options and riders. However, believing that only affluent individuals can afford it might deter many from considering this viable option that can secure their family's financial future. Understanding these myths is essential to avoid mismanagement of funds and to ensure sound decision-making.

Is Whole Life Insurance Really Worth It? Debunking Costly Misconceptions

Whole life insurance has been surrounded by various misconceptions that often lead individuals to question its true value. Many people mistakenly believe that it primarily serves as a savings account, leading them to view it as an unnecessary expense. In reality, whole life insurance offers lifelong coverage and a guaranteed cash value that can be accessed during emergencies or for financial planning purposes. It is essential to understand that the premiums of whole life policies are structured differently compared to term insurance, which can make it seem more costly upfront, but this investment can yield significant long-term benefits.

Another common misconception is that whole life insurance is only beneficial for the wealthy or those with complex financial needs. In truth, its predictable benefits can serve a wide range of individuals, providing not just death benefits for loved ones but also cash value accumulation over time. This can offer peace of mind knowing that your beneficiaries will receive a guaranteed payout upon your passing. Moreover, it is crucial to consider the potential of tax-deferred growth that whole life insurance policies provide, making it a valuable tool for both protection and wealth accumulation.

What You Need to Know: Misunderstandings About Whole Life Insurance That Could Be Costing You

Whole life insurance is often shrouded in misconceptions that can lead to costly mistakes. One of the most common misunderstandings is that these policies are significantly more expensive than term life insurance, which can deter individuals from considering them. While whole life insurance does have higher initial premiums, it's essential to recognize that these costs contribute to a lifelong coverage benefit, as well as a cash value component that can grow over time. Ignoring this aspect can prevent you from making informed decisions about your financial future.

Another prevalent myth is that whole life insurance provides no flexibility. In reality, many whole life policies offer the option to adjust premiums and death benefits as your needs evolve. This flexibility can be a game-changer, allowing you to tailor your insurance to fit your circumstances better. By failing to understand these features, you might miss out on a policy that not only secures your family's financial future but also adapts to your changing life stages.